The delayed AGM, the accounts and the audit

A summary of the issues with the company's approach to the AGM, supported by their own statements.

6/17/20255 min read

The AGM

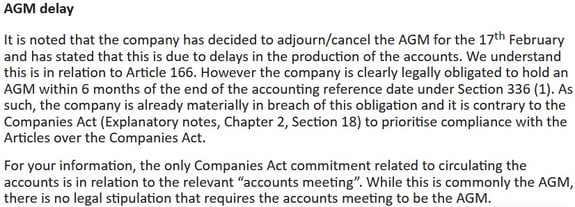

Under the Companies Act, a traded company must hold an AGM within 6 months of the end of the financial year. For PPP, that would give a deadline of 30 September 2024.

Similarly under the Companies Act, a company's own articles cannot override stipulations set out in the Companies Act i.e. no company can elect to operate contrary to UK law.

Under the Company Secretary's guidance for AGMs, a meeting is deemed 'held' if all relevant business has been completed.

As of June 2025 the company has not completed its AGM, now being 9 months in breach of its legal obligations. An initial delay may be somewhat understandable - the death of the former company secretary, alongwith the culmination of the JV with Globabalvision International, and changes to the board are all factors that would impact a small company in its ability to deliver a competent and effective AGM. However, the board has been consistent since January 2025, and elected to actively postpone the AGM scheduled on 17 February.

It's provided rationale for all of this are the delays in the company accounts and completion of the audit, as stated in the 20 June RNS:

"Once the audited accounts for the year ending 31 March 2024 have been signed off by Crowe U.K. LLP, the Company will be looking to hold the Annual General Meeting, which includes seeking approval of the audited accounts."

Similarly, on 30 January:

"As the AGM has been set for the 17th of February 2025, upon advice received, the meeting will be adjourned until such that date as the company is able to present its audited financial statements."

There is no prescribed requirement for accounts to be laid before an Annual General Meeting and approved by shareholders in the Companies Act - clearly companies do this to prevent having to hold two separate meetings, but legally, they are independent requirements. It is unclear what professional advice was received and which party advised them to breach the Companies Act - this has never been communicated by the company.

As seen in the excerpt of a letter to the directors, above, this has been communicated to the directors and company secretary numerous times by various shareholders over the last 6 months, however the company is yet to take action or respond as to why they are prioritising internal company processes over legislative obligations.

Complications as a result of unduly delaying the AGM

PPP's historical approach to resolutions has been to approve for the shorter of a) a duration of 15 months or b) the subsequent AGM. Specifically this relates to resolutions at the 2023 AGM to issue shares and to disapply pre-emptive rights i.e. since April 2025, the company and its directors have no legal authority to be able to enter transactions to issue shares, nor to offer shares in a proportion to existing shareholder proportions and on the same terms.

Clearly this causes issues for the notified GEM agreement and the company's upcoming General Meeting to issue shares at nil value to those previously loaned to the company, and an undisclosed debtor at an undefined price. This would also cause issue for any future fundraising.

Similarly, Stephen Lunn and Olof Rapp are both required to be elected at this AGM and as such, both are operating outside their shareholder authorisations by continuing to act on the company's behalf.

Finally, as flagged here, there exists conflicts of interests that do not appear to have been addressed, or even fully disclosed, by Stephen Lunn. In such cases, ratification by shareholders would typically be a minimum consideration to ensure a director's actions are in line with shareholder expectations.

The accounts and the audit

Despite a long-term suspension from trading, and a lack of of operational activity to manage due to the apparent delays to the JV with Globalvision International confirmed on 1 August 2024, the company has been unable to deliver the accounts in a timely fashion and has continuously delayed the timetable.

The company has made no statements beyond:

"It is worth noting that part of the reason for the delay in producing the audited accounts was due to the lack of records by the Company.

As a result of the commitment from GEM Global LLC SCS ("GEM") referred to below, the board of directors of the Company have now been able to provide Crowe U.K. LLP, the Company's auditors, with a going concern memorandum."

"it is a matter outside of the control of the Board of Directors."

"it has been decided to adjust certain terms and conditions relating to the Placing, to reflect the growing confidence of the Board in the Company's near-term prospects, and in particular, the lifting of the suspension in trading in PPP's shares in the immediate future."

The Board is now confident that all of these outstanding issues will be successfully addressed in the near-term, clearing the way to provide clean titles and access to commence work as soon as practicable, and allowing the restoration of trading in the Company's shares in the timescale outlined above. [prior to end of March]

Further adding to the confidence of the Board, the audit is also now advancing, and the market will be advised as soon as possible in regards to actual and final completion date ."

"The audit is not expected to be finished until the first quarter of 2025 with the consolidated management accounts only being recently completed. This was delayed due to lack of available financial information regarding the US subsidiaries."

These messages conflict with each other and do not align up with communicated timelines, other obligations or common understanding of good business practice. For example, in 20 June, the company has communicated that it has addressed a risk by the auditor around PPP being a going concern. However, at no point has the company notified the market (as required under FCA MAR standards) to notify the market of such fact, nor the reason for such an assessment.

Similarly, incomplete records was noted as a reason for the delay in finishing accounts in December 2024, and yet the company now again refers to this 6 months later as a reason why it is still delayed.

In contrast, in early January, Stephen Lunn and Olof Rapp's confidence in the audit being completed in Q1 was high enough to offer free shares to investors, should this timeline not be met.

Finally, it should not be forgotten that the interim(unaudited) half yearly accounts were due to be issued in December 2024, and failing this, that the company should notify the market and explain the delays. By this time the company had confirmed that it had completed the 23/24 accounts and so it remains unclear why the company cannot meet these minimum standards of administration and compliance.

Empowering shareholders for a brighter future.

© 2025. All rights reserved.

PPPInvestors.org is independent of Pennpetro Energy PLC and is not created by, funded or operated by Pennpetro Energy PLC. Any information or views provided on this website should not be considered as representative of the company's views, nor necessarily supported by the company.